Which is best for you?

When considering a new car for personal use, should you take out a loan or lease a vehicle? You will need to determine what works best based on need, desire, lifestyle, and how much ‘moolah’ you have in the bank.

Comparatively, all car finance, including poor credit car finance options still require a monthly or regular payment scheme. Some financial institutions may offer no deposit down, but carefully read the fine print within your contract. Before we get down to the main business of the article, it might help to explain a couple of things first.

Getting to know the specialised jargon or lingo will help you to understand all of your options and what you are signing up for, i.e. PCP, HP, leasing, and personal loan. (PCP stands for Personal Contract Purchase and HP for Hire Purchase.)

If you want to use your vehicle for business, the criteria of pros and cons may vary considerably, but business-use is not within the scope of this article. Instead, let’s look at the ‘loan or lease’ list of pros and cons to evaluate the best choice for personal-use vehicle finance for you.

Car for Hire

Leasing finance may be the quick-and-easy option for you, but is it the best choice overall?

Pros

Lower car payments per month are available with loans because it is a ‘secured’ loan, meaning that the car itself acts as collateral.

You will usually have lower down payments.

VED stands for Vehicle Excise Duty, a.k.a. ‘car tax’, is factored into the monthly payments so there’s no need to worry over fluctuating rates.

You won’t get stuck with a massive balloon payment.

The opportunity to drive new, more expensive car models for less money in the short run is attractive.

You have the convenience of short-term use.

There’s no getting stuck with a lemon or have to trade it in or sell it on.

Cons

Depending on the length of the lease agreement, you may very well pay more than the vehicle is worth to own.

You don’t have that sense of ownership. The lending company is the ‘owner’.

Liability – You worry about wear-and-tear fees, insurance claims, and being blamed – the added stress of keeping the car in ‘good nick’.

Pay extra for excess miles.

You are bound by a contract for a certain amount of time, and if you are able to break your contract, you will likely be subject to costly penalties.

Purchasing

We all like to feel the sweet success of ownership; it can be a real sense of personal accomplishment, especially when you are starting out in life. But what is really the best for you now? It could be taking out a loan…

Pros

You own the car outright.

It is a chance to build equity in ownership.

Taking out a loan is building/strengthening your credit rating (as long as you stick to the agreed terms and repayment schedule).

Freedom to do what you want with it when it is paid off, e.g. sell it, trade it, pass it down to family, etc., is yours.

Statistically, buying a car is cheaper in the longterm.

You may not need to pay a costly deposit.

There’s no need to offer collateral to receive the loan, as such it is an ‘unsecured’ loan. This makes it less risky to you personally.

Cons

You will be subject to more expensive monthly payments.

You must cover the cost of the repair bills as the car ages.

Depreciation – even driving it off the lot decreases its value, especially if the car is brand new.

It is harder to be approved for finance unless you have a good credit rating (research your options as some financial companies specialise in ‘bad credit’ lending).

There’s no breaking your contract or changing your mind. (However, you might want to look into Part Exchange, as it might be an option to upgrade/change your vehicle.)

Penalties for early settlement (paying off the loan earlier than the agreed timeframe) might be incurred.

Hybrid or Other Options?

No, I don’t mean a hybrid enviro vehicle (necessarily), but two other options you may consider is lease-to-own with hire purchase, and personal contract purchase.

Hire Purchase

With HP, you agree to a fixed monthly payment rate for an agreed term including interest charged, no estimated mileage, and when you have made your last payment and the contract term expires, you will own the vehicle.

Pros

Straightforward contract – you are renting to own the vehicle.

You might have the potential for a lower deposit payment.

It might be helpful to those who do not have the option of an outright personal loan.

Payments cover fixed monthly payments and interest rate.

Mileage is unlimited.

Cons

Higher payments per month than a PCP (below) as the value of the vehicle is factored into the costs.

You are stuck if you need to sell the car but still owe money on it.

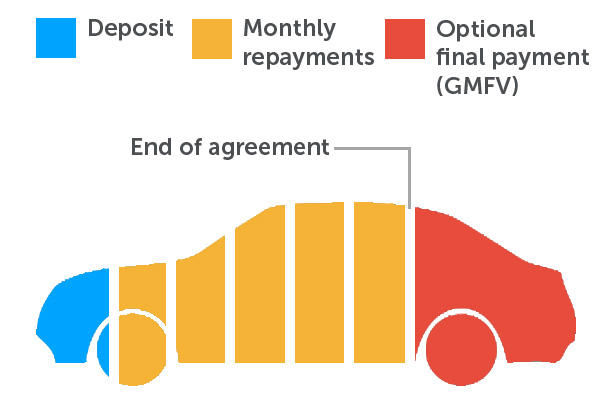

Personal Contract Purchase

If you choose PCP, a payment schedule and fixed mileage are agreed, but you have three options at the conclusion of your contractual term offering you more freedom of choice. You are renting to own if that is what you want to do.

Pros

You have more choice at the end of the contractual agreement to own, trade or return the car.

Monthly payments are generally lower than other finance options (as it is a secured loan).

You can drive away in a higher-spec car than you can otherwise afford.

The option of getting a new, different car after the expiry of your contractual agreement is available if that is what you want to do.

Cons

Payments cover the depreciation rate of the vehicle over the contractual period, but if you do not take care of the car, it can depreciate faster and you will have to cover that cost.

Beware the cost for higher-than-agreed mileage, as the penalties will sting the wallet.

A ‘balloon payment’ is due when the contract expires to cover the remaining balance owed and is sometimes astronomical that people choose not to buy the car but take out another PCP.

The Bottom Line

There are pros and cons to all of the financial agreements available. For your own financial security, you will need to weigh up all of the options against their pros and cons and do your own research before committing to such a weighty financial agreement. May your finances “always be in your favour”.